[ad_1]

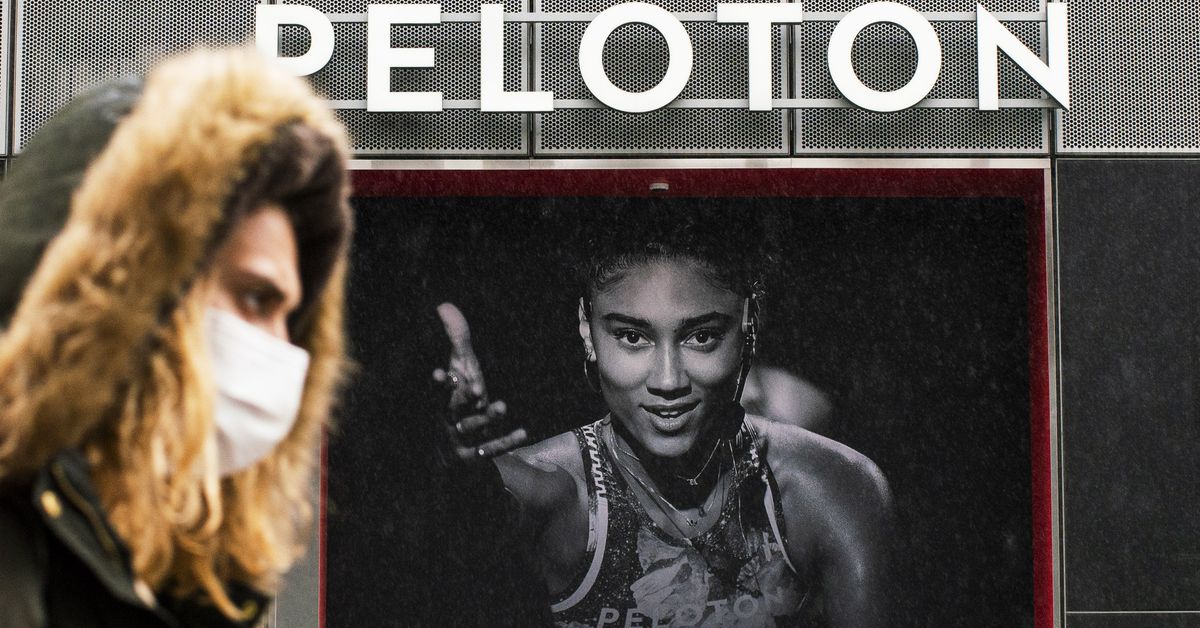

Peloton is spiraling, and its downfall might be a harbinger of actual hassle for a complete business. The at-home digital train firm is one in every of a number of that thrived in the course of the pandemic and promised to vary endlessly how we work out. However now, it’s not clear in the event that they’ll be round to complete the at-home health revolution they began.

There’s no denying that the pandemic made understanding at house extraordinarily well-liked. After gyms had been compelled to shut their doorways, individuals canceled their memberships and invested in train tools and on-line class subscriptions as an alternative. A lot in order that corporations like Peloton couldn’t sustain with demand, leaving many purchasers to attend months for his or her bikes and treadmills to be delivered. However Covid-19 restrictions didn’t final endlessly. Ultimately, when gyms began reopening, individuals stopped shopping for — and utilizing — train tools with the identical enthusiasm that they had within the spring of 2020.

This transition has been brutal for Peloton. Gross sales of latest bikes have slumped, and other people haven’t purchased sufficient of the corporate’s newer merchandise, which embrace two treadmill fashions and weights, to make up the distinction. After shedding $439 million final quarter, Peloton determined in January that it will quickly halt manufacturing of its bikes and treadmills to chop prices, in line with inner paperwork obtained by CNBC. Then, on Tuesday, the corporate stated that it will lay off 2,800 individuals, cancel its plans for a brand new $400 million manufacturing unit in Ohio, and that its CEO, John Foley, would step down. Former Spotify CFO Barry McCarthy will take his place.

Most of the points Peloton confronted had been particular to the corporate. Some buyers had argued that Foley — who led the corporate for a decade — simply wasn’t as much as the duty of scaling the corporate so rapidly. Peloton additionally had a sequence of slip-ups, together with provide chain issues, a really public recall of its treadmills, and a controversial advert marketing campaign.

However Peloton’s demise additionally coincides with a development in additional individuals understanding like they used to do: at gyms. Demand for in-person health lessons and gymnasium memberships has rebounded, whereas Google searches for house gymnasium tools total have continued to fall since their excessive in March of 2020. Foot visitors to gyms has now returned to the identical ranges as January 2020, in line with information from SafeGraph, a geospatial information firm. Planet Health alone stated that, by November, it had recovered 15 million prospects, which quantities to only half 1,000,000 prospects lower than its pre-pandemic peak.

Within the wake of the return to gyms, Peloton’s opponents are beginning to see indicators of hassle, too. Mirror is one in every of them. The corporate sells a $1,495 sensible mirror that streams digital train lessons on the floor of the system as you’re employed out. Only a few months into the pandemic, Lululemon purchased Mirror for $500 million in a bid to capitalize on the large transition to at-home health. Over a yr later, the athleisure model has lower its estimated income expectations for Mirror in half.

“As you realize, 2021 has been a difficult yr for digital health,” Lululemon CEO Calvin McDonald informed buyers in December. “Now we have seen growing pressures on buyer acquisition prices which might be impacting the whole business.”

In the meantime, NordicTrack’s dad or mum firm, iFIT, introduced that it will go public final September, however a month later, it delayed the transfer, citing “antagonistic market situations.” And Nautilus, which owns health manufacturers like Bowflex and Schwinn, additionally reported late final yr that a few of its merchandise haven’t been promoting in addition to they did earlier within the pandemic, although many are nonetheless extra well-liked than they had been again in 2019.

It’s potential that Peloton might discover a path ahead if a bigger firm acquires it. However there are causes to consider that gained’t occur, even with its new CEO. Some activist buyers need a bigger firm to purchase Peloton and have urged a minimum of 19 potential candidates, together with Apple, Netflix, and Lululemon. However these corporations will not be desirous about an costly however area of interest health enterprise. Apple, as an example, is already cautious of shopping for extra corporations and catching the eye of antitrust rules. Netflix isn’t within the system enterprise, and the streaming large has usually averted health content material. Lululemon already has Mirror.

However as Peloton searches for a purchaser, loads of different corporations are constructing streaming platforms for health content material that permit individuals to make use of any tools they need — and for lots much less cash. These companies embrace Apple’s Health+, on-demand house exercises from ClassPass, and tens of millions of health movies on YouTube. These streaming choices are likely to become profitable via commercials or low-cost month-to-month subscriptions with out pushing individuals to purchase specialised tools.

Whether or not different corporations will go the way in which of Peloton stays to be seen. After all, this could hardly be the primary time an at-home health fad has come and gone. Each technology of tech appears to return with its personal spin on the house health revolution, from VHS aerobics to the train tools bought on QVC. This time round, Peloton thought streaming and touchscreens can be the breakthrough to maintain individuals hooked. Sadly for Peloton, the corporate could have simply constructed one other costly clothes rack.

This story was first revealed within the Recode e-newsletter. Enroll right here so that you don’t miss the subsequent one!

[ad_2]

Source link

{kind=link}